Some 8 years ago, 2018, I calculated that a fair price for Bitcoin was likely $11,000, with a maximum of perhaps 4x more, $44,000. I used Fischer’s formula from my economics textbook, perhaps the only useful formula there. It’s based on the idea that the total currency value times the speed of money has to match the value of the things people buy with it. See the analysis here. Based on this formula, you see that, if you print more money, you get inflation — a concept that seems forgotten today.

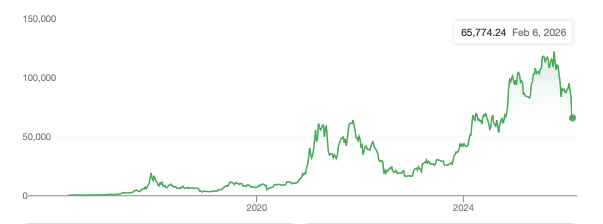

It’s eight years later, and while there has been some inflation in the price of everything, the price of bitcoin has outstripped most everything else. After years of Bitcoin staying in the price range I’d suggested, it jumped to over $120,000 in 2025 before dropping back to $70,500. I figured I should revisit my calculations, and again find about the same result corrected for normal inflation: a “true value”, of <$33,300. I show why I value it this much, and share why, I think the market is wrong.

Bitcoin has only one “legitimate” use, as best I can tell, and that’s for illegal activities, like paying $6 million dollar to ransom Nancy Guthrie. The problems preventing a high bitcoin valuation, IMHO, are that there is not that much illegal trade, and there are other ways to pay for illegal things. Suitcases of cash can be used, or gold coins, or artwork. These are just as safe as bitcoin, and almost as easy to ship. For legitimate business, almost any pay method is better: easier, faster, and more secure.

Most people, I suspect, don’t use their bitcoin at all. They buy it as an investment, or as a gambling speculation, but that’s a zero-sum gamble, somewhat worse than gold, since gold have value above trade. Having no value aside from trade, Bitcoins are only as valuable as their use is.

One of the main use of bitcoin transactions is to avoid tariffs on legitimate goods – I explained how that was done, previously. I estimate the magnitude of this business to be $500 billion or so per year. The US collected about $220 billion in tariffs last year on a trillion dollars of trade, and I find it hard to believe that Bitcoins cover more than another 50%. Add to this, bitcoin is likely also used to hide payment for illegal, sanctioned oil from Iran and Russia. There are other ways to do this, but let’s assume it’s all bitcoin-trades. Since this oil trade seems to be about 8 million barrels per day, and since oil costs ~ $70 barrel, I calculate a business of $200 billion in world oil. Add a few more items that you don’t want traced: drugs, weapons, for a total of maybe $200 billion, add $100 billion to over-throw countries and for a kidnapping or two, and I find a total bitcoin trade of $1 trillion, or $1000 billion. If a bitcoin trades 1.5 times per year (a fairly low rate) the total value of bitcoin is $1000 billion /1.5 = $667 billion. Divide by the total number of bitcoins, 20 million, and I calculate a value of $33,300 per bitcoin or less.

A lot more value in bitcoins trade per year, about $10.5 trillion. The average Bitcoin price is three times higher than I estimate and it is spent 7.5 times per year. Most of this is churn: investment, plus some legitimate purchases based on illegal activity, like when the drug dealer buys a new car in Panama, but these sales are consequences of the other, illegal sales. I figured that each Bitcoin was used for an illegal purchase only 1.5 times per year because normal money is used ~4.5 times per year.

I should note that some illegal activity is done in US dollars, including most drug deals, and when Obama bought back US soldiers kidnaped by Iran, using bales of € 500 notes, and some is done using gold or silver. Bitcoin is easier to move but large quantity moves can still be traced, and there are other crypto currencies too. Bitcoin transactions aren’t free, either, or particularly cheap. And it takes time to process the transfer of bitcoin numbers, milliseconds, but that’s slow in world commerce. As a result. I don’t see bitcoin being used for legitimate business, and unless it can break out of the black market, the value seems limited to $33,300, and probably less.

Robert Buxbaum, February 15, 2026. Gold, by the way, is similarly overvalued, in my opinion. Like bitcoin, it’s a non-dividend investment that’s expensive to trade, but at least it has some other uses, as jewelry, and in electronics. Besides, it’s relatively hard to steal a billion dollars in gold from a Swiss bank – harder than stealing $1B in bitcoin.

{kind=link}

{kind=link}