One of my favorite presidents is James K. Polk. While running for president he claimed we would do four major things –and do them as a one-term president. He then did them, and left office — and died 103 days later at the age of 53. Mr Polk’s four stated objectives were: a reduction in the tariff, an independent treasury, settlement of the Oregon boundary dispute, and acquisition of California. Acquisition of California required admission of Texas, plus a war with Mexico and a cash payment, but he was ready. Settling the Oregon border required a compromise and a cash payment. But he did it and more. Modern professors are not happy with Polk, ranking him far below Obama, Kennedy, or Adams, but his aims were good, and he got hem done. Few presidents do that, and even fewer left office if they had the power to stay. No professor I know has ever willingly left if he had the power to stay, and didn’t have a better job to go to.

I believe that the clarity of Polk’s four objectives was the reason he was a candidate at all, and the reason he won the election, and also the reason he achieved the objectives. There is a magic in clear objectives, repeated often, I find. It’s a formula that got Trump elected that few seem to understand: “Make America Great Again.” “Build the Wall”, “Drill baby Drill” “Deport illegals” “Tariffs. ” Like these ideas or not, you know Trump’s aims. Also, you know that, if. you oppose them, you oppose him. Trump’s pastor, Norman Vincent Peale promoted this approach, one I’ve thought of trying myself. I suspect that Polk died so shortly after leaving office because he had no further goal beyond relaxing; bad water hurt him too.. I suspect that Trump will die shortly after leaving office too- from lack of purpose.

Polk wasn’t expected to be a candidate, but was a “dark horse”, ex-governor of Tennessee, who had lost his past two elections. Martin Van Burin was expected to be the Democrats’ candidate, but he opposed slavery, and most Democrats were for it. What’s more, he was opposing annexation of Texas, at least south of the Nueces River, and many Democrats were for, as were some Whigs.

Polk was pro-slavery, as was the Whig candidate, Henry Clay. But Polk said repeatedly that he would annex Texas — all the way to the Rio Grande, “no matter what any Mexican said.” He also said he’d fight for California and all of Oregon too: “Fifty four forty or fight”. You might not agree with this, Grant did not, but you knew where he stood. And Polk said he’d serve only one term. Thus, if you didn’t like him, he’d be gone in four years. After a few ballots, Polk became the Democratic Party candidate, with George Dallas as his VP. Like Polk, Dallas was pro Texas – they eventually named a city after him. Clay was Polk’s main opposition, anti Texas, and more vague about everything else.

At first John Tyler, the incumbent, also ran against Polk, but when he saw he was losing, he dropped out to help Polk. Also running for president, 1844 was Joseph Smith, the Mormon founder-profit. he ran as an independent because God told him to. He was shot multiple times, and died while campaigning. Finally there was James G. Birney, the Liberty party candidate. He gained few votes running on an abolitionist ticket. It’s been speculated that Polk won because Birney split the Whig vote. My take is that’s unlikely: Clay was pro-slavery. Polk’s win, I think, was in the power of his clarity.

Once elected, Polk first moved to annex Texas, something he achieved with the help of expresident John Tyler. Tyler sent his Secretary of State, Abel Upsher to negotiat an annexation treaty with Sam Houston, but the Whig-controlled congress rejected it. After the election, Tyler resubmitted the treaty to the new, Democrat-controlled congress, and got two versions passed. The house passed a pro-slavery version, while the senate, pushed by Thomas Hart Benton (a favorite of mine) produced an annexation treaty that divided Texas in half, with a pro-slave and an anti-slave half. Polk liked the pro-slave, House version, returning it to Texas in his first week in office. He instructed the Texas legislature to accept it unconditionally, with no change so he could submit it directly to the Senate. The Texans did so, and congress approved this version later that year. Texas entered the union as one, large, slaveholder state.

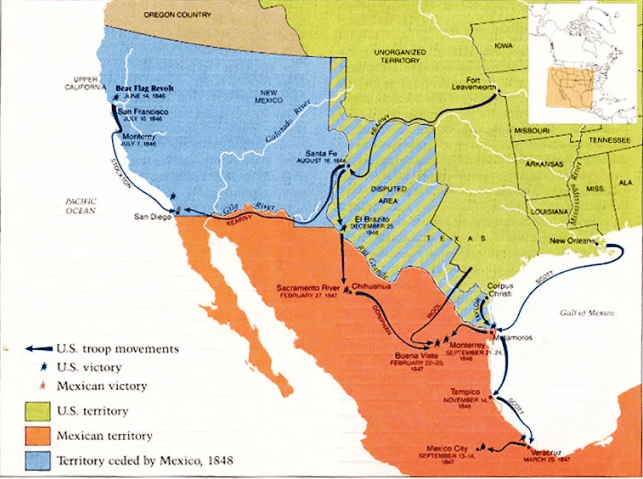

With annexation not yet ratified by congress, Polk sent a diplomatic mission to buy California from Mexico along with all of the disputed Texas territory and everything in between for $25 million. Mexico refused, so Polk invited war. He sent 4000 soldiers into disputed Texas territory south of the Nueces River, under command of General Zachary Taylor. Mexican forces attacked them in April 1846, and Polk declared war. The war lasted to 1848, winning all the desired lands including California, and achieving a release of any rights Mexico might have on Oregon.

The next Polk goal was resolution of the Oregon dispute, ideally with us getting all of it: land that included the current states of Washington, Oregon, and Idaho, plus the Canadian Provence of British Columbia. Britain and Russia also claimed this land, so Polk’s first step was to buy off Russia. The British said they’d fight, noting that they had a larger army and navy and that the US was already at war with Mexico. Polk’s response was to back settlers going to Oregon. Americans had started migrating to Oregon in 1843. In his inaugural address, 1845, Polk said he would defend them “against the British and Indians.” By 1846 Britain recognized the difficulty of fighting US settlers so far from home. On June 15, they agreed to a deal that split the territory along the 49th parallel, giving the US the lower half, except for Vancouver Island, thus allowing Britain an opening to the sea. This deal had been proposed by Edward Everett, Tyler’s minister in London. Polk gave up nothing, beyond an informal agreement to lower tariffs on British goods, something he aimed to do anyway. It’s generally thought that Polk’s willingness for war allowed him to achieve so much without fighting. Polk said, in his inaugural, March 1845: “The world has nothing to fear from military ambition in our government,” a statement that clearly means the opposite of what it claims to say.

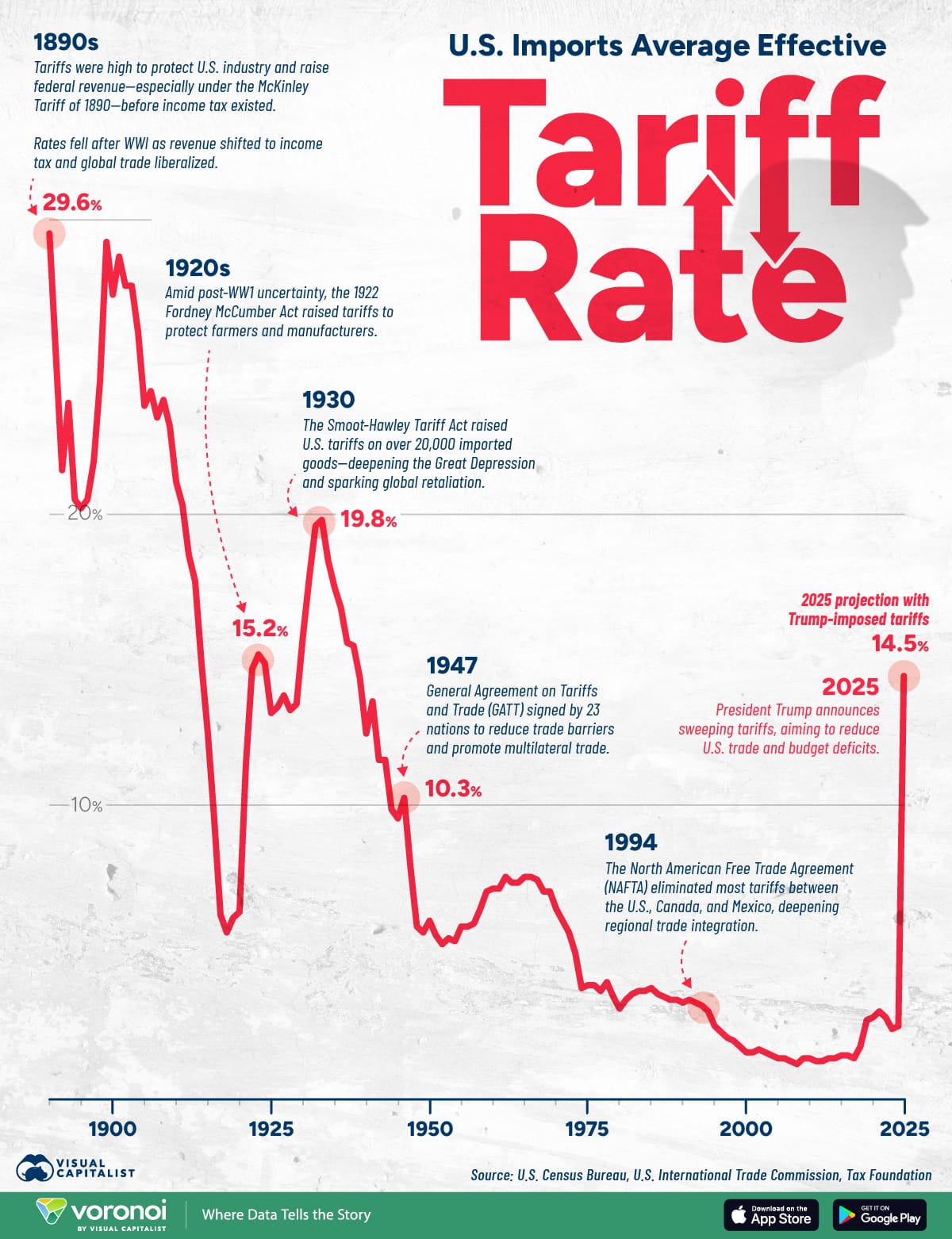

Polk’s third goal was lowering the “Black Tariffs”. High and uneven, they were 32% on average, with cut-outs to help specific, northern businesses. Polk’s secretary of the treasury, Robert Walker negotiated a flat advalorum tariff of 25%, with luxury goods, tobacco and alcohol tariffed higher. The “Walker tariff” bill was passed July, 1846, one month after the Oregon agreement. The British, reduced their “corn tariffs” against US grain, benefitting both countries. Our tariffs average 17%, currently, with many cut-outs. I think our tariffs should be more like the Walker tariff, perhaps 20% and simpler.

Polk’s 4th campaign promise was establishing an independent treasury. This was done to weaken “pet” banks, and stabilize the economy. The treasury would now hold all US assets; they would issue most currency, and would pay people directly, either in specie (gold or silver) or notes of debt. Independent banks could still issue notes, but only in amounts over $20. Polk passed this bill August 6, 1846, one week after the Walker Tariff bill. With this, Polk had already achieved all of his goals except California by the mid-term elections, 1846.

Having achieved so much, Polk set out to buy Cuba, but Spain said no. Some other accomplishments: opening the U.S. Naval Academy and the Smithsonian Institution, overseeing the groundbreaking for the Washington Monument, and the issuance of the first United States postage stamp. By the summer of 1848 Polk confirmed that he was satisfied and would not run for re-election. In his address to congress, December 1848, he said, “Peace, plenty, and contentment reign throughout our borders, and our beloved country presents a sublime moral spectacle to the world.” …. “I am heartily rejoiced that my term is so near its close. I will soon cease to be a servant and will become a sovereign.” I trust that was met with applause.

Robert Buxbaum. February 6, 2026. Edward Everett would go on to make the better received speech at Gettysburg. The officer who commanded the 4000 man Texas force, Zachary Taylor, became president in 1849. Like Polk, he died of bad water with too little alcohol added.

{kind=link}

{kind=link}

{kind=link}

{kind=link}