For better or worse, the folks who run for library board and school board are a bizarre lot of political weirdos. It takes a lot of work and time and money to run for these boards, and you have to endure endless insults. For what? If you win, there’s no pay, and you get to sit through long, boring meetings. Because of this, almost everyone, who choses to run for these positions is a weirdo with a bering desire to either ban some book or idea, or to promote them. The rest are little better: developers who want to expand buildings and grounds. I don’t think this problem is unique to the US, or new. That’s just the way it is, and has always been. Noah Webster complained about this in the early 1800s. The net result is large schools – larger than they have to be – and many banned books, plus a preponderance of really perverted books.

In terms of teaching, I find myself on the side of classic books that are fairly non-sexual. That’s because I read them. Many people find them dull. I suspect that the students would prefer more modern and racier fare, or no books at all, but what do I know. In terms of library purchase, I like variety, but virtually no library works that way, either the board are a band of perverts pushing weird sex on under-age kids, or they are blue-noses who want to keep Shakespeare from the shelves. I also claim to prefer a diversity of opinions both in the classroom and in the library, but I suspect that, I’m likely to favor my own opinions over others. Below is the selection of banned books that the “don’t censor” organization wants on all shelves, all gay or transgender, as best I can tell. .

These books are banned in some counties K-12 public schools all are gay or transgender. While I’m not a fan of banning, I’m doubt these are the books to push. Pecksniffs on every side.

Sometimes very good books get banned, for no reason, or modified. This was done with Bowdlerized Shakespeare, for example. Once banned, it’s a lot harder to un-ban a book than it is to ban it. You’d have to get an unbanning committee together, almost impossible, and get them to read all the books. They’d have to make a coherent argument for their merits, and then have some vote. It would help to have balanced boards, but I fear that’s not likely/ possible. If nothing else, I’d like a time limit to banning: any banned book stays banned for only 12 years, or so.

I ran for school-board one year, by the way, and lost. I campaigned on math and science education, and less money for ever larger buildings and grounds. Against AI teaching of math and reading, claiming that math education suffers,. I also like cursive handwriting, something I consider an art form. I lost. You can find my Ballotopedia page if you’re interested.

Innovation is the special sauce that propels growth and allows a country to lead and prosper. The current Nobel prize believe that innovation powered the Industrial Revolution, causing England to become rich and powerful, while other nations remained poor, weak, and stagnant. Similarly, Innovation, they believe is why 19th century Japan rose to defeat China, and propelled China’s 21st century rise. But why did they succeed when others did not. What could the leader of a country do to bring power and wealth through innovation. Improved education seems to help; all of the innovation countries have it, but it is not the whole. Some educated countries (Germany, Russia) stagnate. An open economy is nice, but it isn’t sufficient or that necessary: (look at China). That was the topic of this year’s, 2025 Nobel prize in economics to Mokyr, Howitt, and Aghion, with half going to Joel Mokyr for his insights, historical and forward looking, the other half going for economic modeling. I give below my understanding of their insights, more technical than most, but not so mathematical as to be obtuse the normal reader..

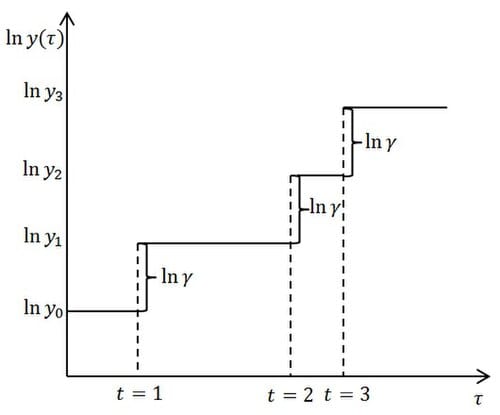

The winners hold that innovation, as during the industrial revolution, is a non-continuous contribultion caused by a particular combination of education and market opportunity, of theoretical knowledge, and practical, and that a key aspect is depreciation (destruction) of other suppliers. Let’s start by creating a simple, continuous function model for economic growth where growth = capital growth, that is dK/dt. K, Capital, is understood to be the sum of money, equipment, and labor knowledge, and t is time with dK/dt, the change in K with time modeled as equal to the savings rate, s, times economic activity, Y minus a depreciation factor, δ, times capital, K.

growth = dK/dt = sY − δ K.

Innovation, in the Howett model, is discontinuous and accumulative. It builds on itself.

For the authors, Y = GDP + x, where x is the cost of outside goods used. They then claim that Y is a non-linear function of K, where K is now considered a product of capital goods and labor K = xL and,

dY/dK = AKα + γ where 0< α <1, and where γ is the contribution of innovation and/or depreciation. The power function, as I understand it, is a mathematical way of saying there are economies of scale. The authors assume a set of interacting enterprises (countries0 so that the innovation factor, γ for one country is the depreciation factor for the other. That is, growth and destruction are connected, with growth being a function of monopoly power — control of your innovation.

According to the Nobel winners, γ is built n previous γ as shown in the digram at right. It can not be predicted as such, but requires education and monopolistic power. The inventor-manufacturer of the typewriter has a monopolistic advantage over the makers of fountain pens. Innovation thus causes depreciation, δ K as one new innovation depreciates many old processes and products. If you add enough math, you can derive formulas for GDP and GDP growth, all based on factors like A and α, that are hard to measure.

GDP = α(2α/1−α) (1-α2)A L,

Thus, GDP is proportional to Labor, L and per-capita GDP is mostly an independent function related to economies of scale and the ability to use capital and labor which is related to general country-wide culture.

The above analysis, as I understand it, is in contrast to Kensyan models, where growth is unrelated to innovation, and where destruction is bad. In these Kenysean models, growth can be created by government spending, especial spending to maintain large industries with economies of scale and by spending to promote higher education. The culture preferred here, as I understand is one that rewards risk-taking, monopoly economics, and creative destruction. Howitt, and Aghion, importantly codify all this with formulas, as presented above that (to me) provide little specific. No great guidance to the head of a country. Nor does the math make the models more true, but it makes the statements somewhat clearer. Or perhaps the only real value of the math is to make things sound more scientific see the Tom Lehrer song, Sociology.

This insight from movie script by Grham Green suggests to me that progress may not be the greatest of advantages, perhaps not even worth it.

This work seems more realistic, to me, than the Keynesian models Both models are mathematically consistent, but if Keynes’s were true, Britain might still be on top, and Zambia would be a close competitor among the richest countries on earth. Besides these new fellows seem to agree with the views of Peter Cooper, my hero. See more here.

Writing all this reminds me that the fundamental assumption that progress is good, in not necessarily true. I quote above a line that Orson Wells, as Harry Lime, ad-libbed for the movie, “The Third Man.” Lime points out that innovation goes with suffering, and claims that Switzerland had little innovation because of its stability. Perhaps then, what you really want is the stability and peace of Switzerland, along with the lack of domination and innovation. On the same note, I’ve noticed that engineering innovators often ruin themselves dining in ruin, while the peaceable, stable civil engineers live long pleasant lives of honor.

Robert Buxbaum, November 16, 2025. A note about Switzerland is that was peaceful and stable because of a strong military. As Publius Vegetius wrote, Si vis pachim para bellum (if you wish of peace, prepare for war).

What makes something elite? For elite colleges and academic journals, a large part is selectivity, the lower fraction of people who can go to your college or publish in your journal, or earn your credential, the more selective, thus the most elite. Harvard, boasts that “the best” apply, and of these, only 3% get in. Thus Harvard selects for the top 1%, or so they claim. These are not selected as the brightest, or most moral or motivated, but by a combination: they are the most Harvardian.

The top 20 most selective US colleges, 2022-23 according to Nathan Yau, FlowingData.com

Selectivity is viewed as good. That this 1% can get into Harvard makes the students elite and makes Harvard desirable. Some lower-class Ivy colleges (Columbia, for example) have been found to cheat to pretend higher selectivity; they’ve exaggerated the number of people who apply so they can inflate their rejection rate, and justify a high tuition, and presumably a high salary for their graduates. And it’s self-sustaining. Generally speaking, college professors and high-powered executives are drawn from elite institutions. Elite grads pick other elite grads as their way to get the best material, with the best education.

By this measure, selectivity, The Journal of Universal Rejection is the most elite and best. It’s the journal you should definitely get. The reject every article submitted on every subject. They are thus more elite than Harvard or Cal Tech, and more select than the quorum of US presidents, or Olympic gold winners, or living Chess champions, and they got there by just saying no. Many people send their articles, by the way, all rejected.

My lesson from this, is that selectivity is a poor metric for quality. Just because an institution or journal that is select in some one aspect does not mean that it will be select in another. Top swimmers and footballers rarely go to Harvard, so they have to pick from a lower tear of applicants for their swimming and football teams. It’s the same with the top in math or science, they apply to Cal Tech, with the rejects going to Stanford or Princeton. As for top chess players or US Navy Seals, a Harvard degree does nothing for them; few seals go to Harvard, and few Harvard students could be Seals. Each elite exists in its own bubble, and each bubble has its own rules. Thus, if you want to be hired as a professor, you have to go to the appropriate institution, though not necessarily from the top most selective.

From Nature, 2024. 20% of all academics come from just 8 schools, 40% come from the top 21.

As for journals to read or write in, an elevated reader like you should publish where you can be read, and understood, and perhaps to change things for the better, I think. Some money would be nice too, but few scientific journals offer that. Based on this, I have a hard time recommending scientific journals, or conferences. More and more, they charge the writer to publish or present, and offer minimal exposure of your ideas. They charge the readers and attendees such high fees that very few will see your work; university libraries subscribe, but often on condition that not everyone can read for free. Journal often change your writing too, sometimes for the better, but often to match the journal outlook or style, or just to suggest (demand) that you cite some connected editor. JofUR is better in a way, no charge to the author, and no editorial changes.

Typically, journals limit your ability to read or share your work, assuming they accept it, then they expect you to review for them, for free. So why do academics write for these journals? They’re considered the only legitimate way to get your findings out; worse, that’s how universities evaluate your work. University administrators are chosen with no idea of your research quality, and a requirement of number-based evaluation, so they evaluate professors by counting publications, particularly in elite (selective) journals, and based on the elite (selective) school you come from. It’s an insane metric that results in awful research and writing, and bad professors too. I’ve come to think that anyone, outside of academia, who writes in a scientific journal is a blockhead. If you have something worthwhile to say, write a blog, or maybe a book, or find a free, open access journal. In my field, hydrogen, the only free, open access journals are published in Russia and Iran.

And just for laughs, if you don’t mind the futility of universal rejection, there’s JoUR. Mail your article, with a self addressed return, or email it to j.universal.rejection@gmail.com. You’ll get a rejection notice and you’ll join an un-elite group: rejected, self effacing academics with time on their hands.

ROBERT BUXBAUM, January 16, 2025. If, for some reason, you want to get your progeny into an elite college, my niece, a Harvard grad., has a company that does just that, International College Counselors, they help with essays, testing, and references, and nudge your progeny to submit on time.

Few people learn cursive these days with any skill or speed. It’s a shame. This is a form of traditional art and communication. Handwriting is a slower way of writing, that leads to a different type of letter or essay. The sentences are, typically longer, and the words more expressive because the experience of writing and reading cursive is more expressive than with text. The emotional state and energy of the writer comes through the cursive writing, because the writing itself is a form of creative art, adding to the words.

Send a letter or a post card, and you’ve sent a work of art. You’ve communicated words, or course, but far more than with a text or email. First off, there is the picture on the card. You bought that card, or took the picture. Then there is the art of how many words you use. Each letter is directed to only one person, not to 100 as with a text. As a result, people will keep your letter or card far more than they will not keep a text an email. It is more from you, and more to them. You are likely to put more (or different) things in: experiences and feelings that don’t go into an email or text-letter. The size of your writing communicates and even your cross-outs are part of a cursive communication. With email or text, there are no natural cross outs, and you can send the same letter to 100 people, so you write more blandly, with an eye for eventual reuse for someone else. A cursive note is intended for only one person, the one recipient, and this affects both the words, and the form of the words.

Cursive also lends itself to adding a small sketch or doodle. This becomes part of a personal part of the art in a way that does not fit with normal text. It’s calligraphy and conceptional art, an important part of education, and a continuation of western culture. In normal texts, some people have come to add emojis or GIFs, but these are nowhere near as personal or expressive. The cursive letter or note is personal and spicy. It’s an important art form, at least a valid an art form as any that could be taught in school, and it should be.

Robert E. Buxbaum, Sept 1, 2024. I’m running for school board, and like the idea of teaching basic knowledge as a foundation of creativity. One of these basics, I think, is cursive writing.

Jewish education is a mess according to the Times. Most anyone outside it, who’d look in would agree: Ancient books, pre-science outlooks, anti-inclusive, and taught in a garble of languages, Yiddish, English, Aramaic, Hebrew. The New York Times has runs regular editorials claiming that Jewish education robs children of a future, or an entrance to society, producing adults who know nothing of geometry or higher math, or modern history, incapable of voting intelligently in today’s elections (they often vote Republican). The Times’s experts, are often the products of this education, but claim to have risen above it, only because of extra work. As a proof, they often cite the Talmud as a source of useless knowledge of ancient Jewish law, rejected Bible history, and only the most basic views of math. By way of a response, I’d like to quote something I’d heard in synagog a couple of weeks back:

“I’m so glad that I learned geometry in school, and not taxes. It’s really come in handy this parallelogram season.“

The speaker was an accountant, and the point of the joke is that there is no parallelogram season. There is a tax season, though, and tax law follows a bizarre logic that is not geometric, but is somewhat talmudic. As for the useless languages, they are all in use, both as spoken languages and written languages, no less useful than Latin, and certainly more alive. There are currently 5 yiddish-language newspapers being published in New York alone, see below. They compete with each other for readers, while competing also with the Times, the Post, and with another ten or more Hebrew and English journals, several of them Jewish, either published on paper or as web-journals. People read them, though the Times prefers to ignore their existence.

There are five newspapers published currently in Yiddish in New York. The Forward (Tony Curtis and duck) and the Vort are left-leaning, the Algeminer, the Blat, and the Zeitung, are more right and center. There is a readership. Why a duck?

And that brings us to the subject matter, Talmud. Much of Jewish learning is Talmud, either distilled or pure, study of a set of books written between 1000 and 2000 years ago in Israel, Babylon, and France mostly, with commentaries from Spain, Morocco, Egypt, Germany, and Poland. Those who learned talmud tend to find it useful. The legal organization and approach resonates to them in the understanding of taxes, contracts, building, damage assessment, marriage, ethics, even in dealing with alcoholism. Talmud is so useful that it’s common for working, orthodox Jews to continue their learning it throughout their lives. A common practice is to learn a page every day in synchrony with other Jews. Today’s page, when I started writing this post, was Nazir 10. It includes a talking cow, just the sort of section that the Times likes to cite to show the uselessness of it all. I’ll forgive their lack of understanding, but not their laziness for not even bothering to try to understand.

Nazir 10 begins by saying: “If a cow says, ‘I will be a Nazir (that is, I will give up wine for a month) if I stand up’. Then, if it gets up, one school of rabbinic thought (Bais Shammai) says he is a nazir. Another school of thought (Bais Hillel) says he is not a nazir.” The page goes on to speak about taking doors, but I’ll stop here after the first 2 sentences and will try to explain what the Times does not care to examine.

Notice that cows are female, and they typically don’t speak, but here you find a “he” who might have to give up wine. This “he”, this male, is understood to be a person looking at the cow, likely a person with an alcohol problem. He sees a cow lying on the ground (in the mud figuratively) and identifies it to himself. That is, he sees himself lying in the mud. He thinks it’s impossible for the cow to get up because he imagines that he himself can not get up. (This is just the Talmud’s way of discussing things). According to Bais Shammai, the person is understood to have said to himself, “if that cow can get up, I will take it as a sign that I can get up, and I will take it on myself to avoid wine and wine products for a month.” Now, according to Bais Shammai, if the cow gets up, the man is obligated to stop drinking for a month.

“I love television, and find it very educational. When someone turns it on, I go read a book.” G. Marx

Bais Hillel says he is not obligated at all. They say that a drunk who wants to change, must do more than be inspired, he must make a real verbal commitment. He must verbally obligate himself to give up drink. We follow this latter opinion, but learn Bais Shammai’s view too, because there are important ideas about self-identity.

Those are just the first two lines of the page. In secular school, you learn stories too, sometimes stories with talking animals, but these are usually modern stories, where the challenges are external, bullying say, but in a sense such stories are sanitized. The internal demons are removed, and these are often the hardest to battle. Even dealing with external problems is often pushed on an external authority, a teacher usually. You are considered to be too weak to deal with a problem. Sometimes that’s true, usually there is at least some part you could deal with. The lack of self-obligation leaves modern school stories flat. Few kids enjoy them, or feel they get anything from them. A result in Detroit is that schools have <50% attendance. Kids leave barely literate with appalling math skills. We blame the teachers and the subject. It’s the book: Sally has 15 tomatoes and wants to give 4 to a friend, how many will she have left? is this relevant? Does this excite?

Talmud teaches some logic, some math, and some geometry, but only for measuring distances and volumes, the application that geometry was named for (geometry = measuring the earth). They learn the rest as needed, and often learn quite a lot.

As Groucho Marx said: “My education is self inflicted.”

The products of Jewish education become successful, often in business, hiring their better-educated brothers. Some become lawyers, accountants, writers, businessmen, or psychologists — more than our share in the population — or mathematicians and scientists. Some even excel in academics or journalism. The Times does not mention this.

Groucho, Chico, Harpo, and Karl Marx

My three children all went to Jewish, religious school and got the education that the Times calls abuse. So far, my son (31) has two masters degrees, both in artificial intelligence/ computer science. My older daughter (28) is getting her PhD in Psychology, and my younger daughter (23) is working on her masters in epidemiology. I suspect they benefited from the education. My suggestion to the Times, is in another Marx quote: “If you find it hard to laugh at yourself, I would be happy to do it for you.”

Robert Buxbaum, March 1, 2023. “History may not think with its feet, but it certainly doesn’t walk on its head.”– Karl Marx, the less-funny, Marx brother. Jewish educated, he became a journalist.

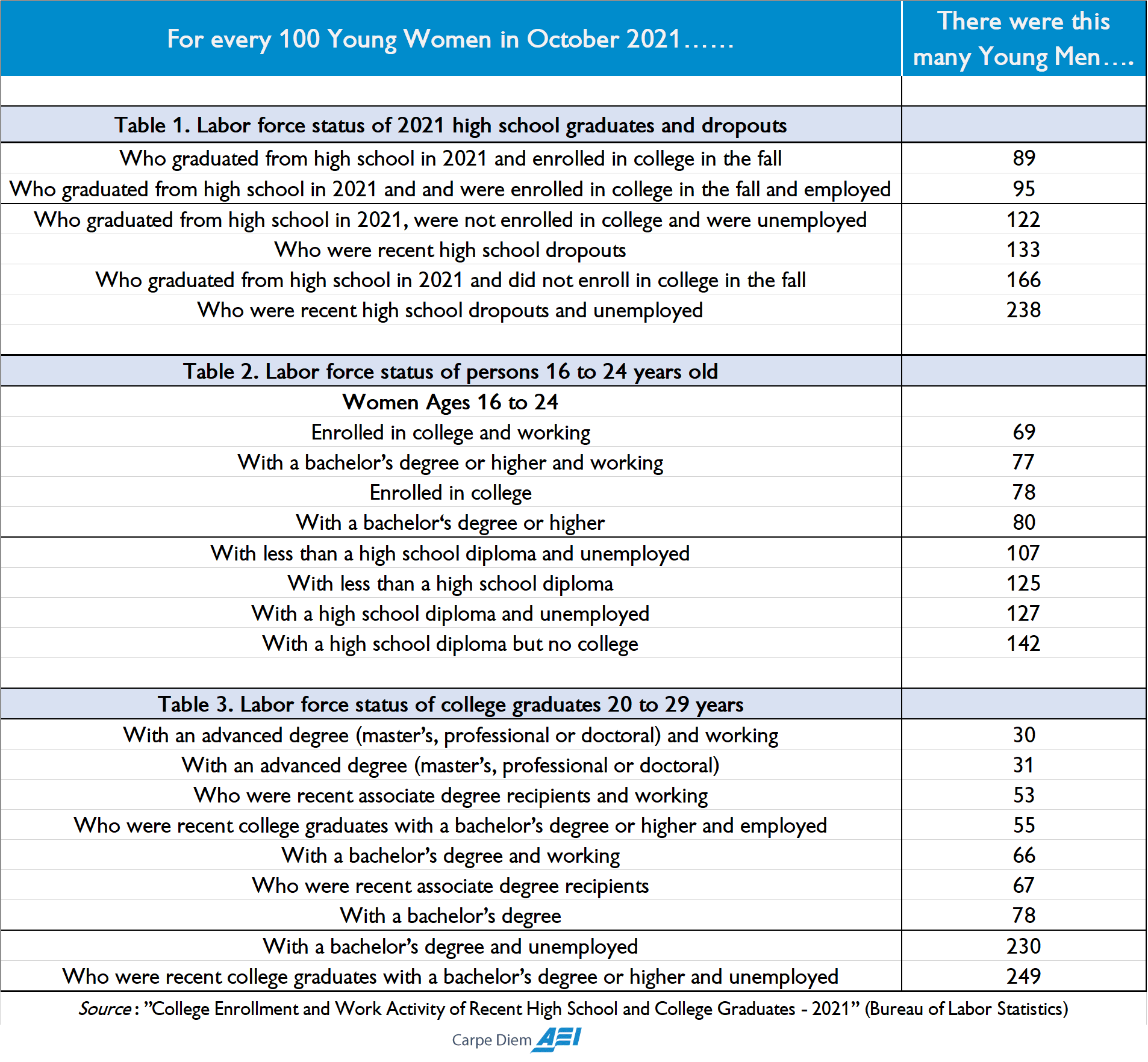

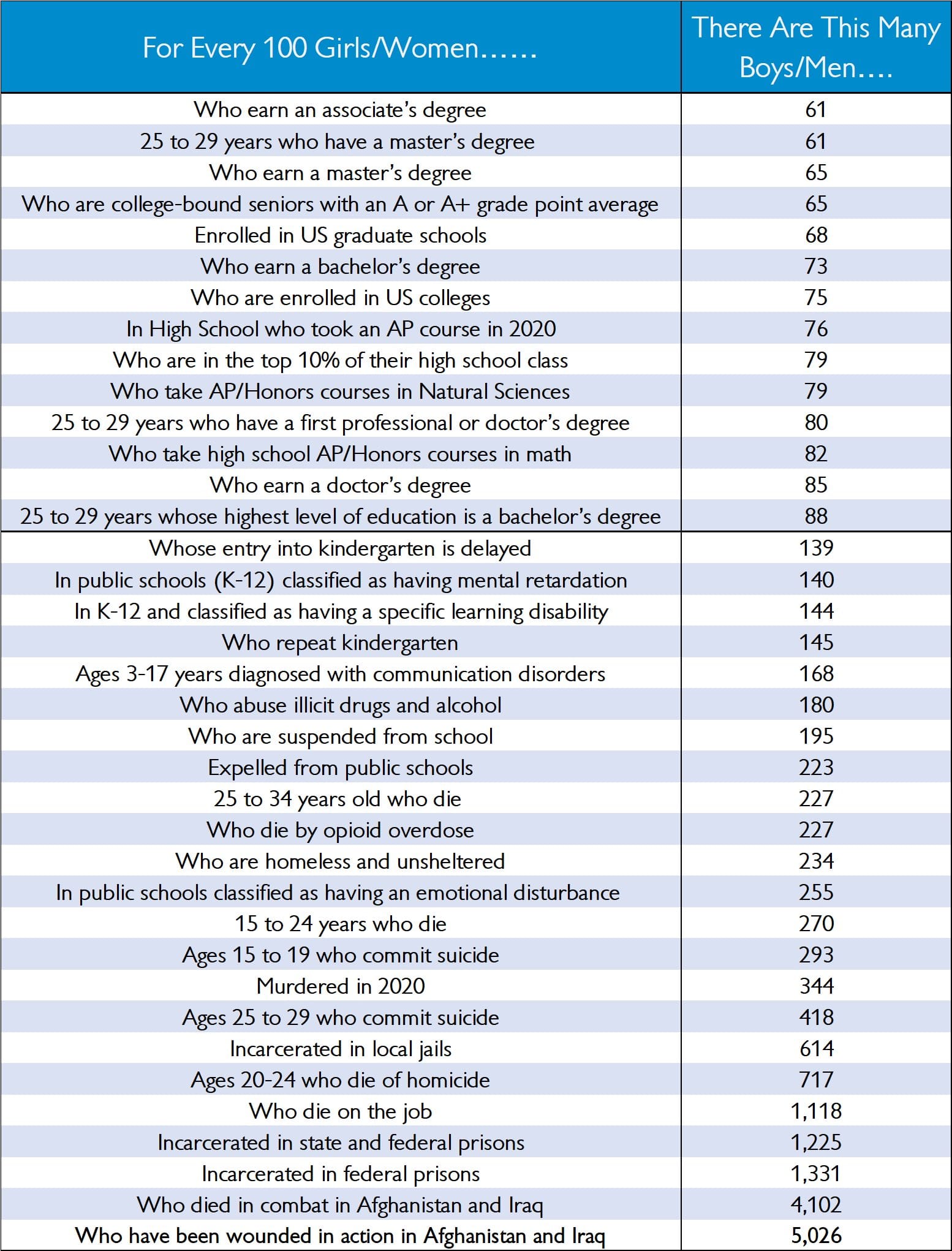

When I began college in 1972, the majority of engineering students and business students were male. They from the top of their high school classes, and from stable homes mostly; they went on to high paying jobs. Boys also dominated at the bottom of society. They were the majority of the criminals, drug addicts, and high-school dropouts. Many went off to Vietnam. Some, those who were handy, went to trade schools and a reasonable life, productive life. Society did not seem bothered by the destruction of boys in prison, or Vietnam, or by drugs, but there was an outcry that so few women achieved high academic levels. A famous presentation of the problem was called “for every 100 girls.” An updated version appears below showing the status as of October, 2021. A more detailed version appears further down.

From the table above, you can see that women are now the majority of those in college, the majority of those with a bachelors degree or higher, and a majority of those with advanced degrees. Colleges added special tutoring, special grants, and special programs. Each college had a Society of Women Engineers office, and similar programs in law and math. All of these explicitly excluded men or highly discouraged their presence. The curriculum was changed too; made more female-friendly. Dirty, and physical experiments were removed, replaced with group analysis of the social interactions — important aspects of engineers that boys were far-less adept at doing well. Perhaps society and engineering is better off now, but boys (men) are far worse off. This is particularly seem by the following chart, looking at the bottom. Boys/men provide the vast majority of the prison population, of those diagnosed as learning disabled, of those expelled, or overdosed, and among the war dead.

I’ve previously noted that a majority of boys in school are considered disruptive, and that these boys are routinely diagnosed as ADHD and drugged. It is not at all clear that this is a good thing, or that the drugs help anyone but the teacher. I’ve also noted that artwork and attitudes that were considered normal for boys are now considered disturbing and criminal like saying I wish the school was blown up. The cure here, perhaps is worse than the disease. I’m not saying that we should encourage boys to say such things, but that we should acknowledge a difference between an active and a passive wish. And we should find a way to educate boys/men so they don’t end up unemployed, addicted, or dead. Currently boy, particularly those at the bottom are on the scrap-heap of society.

Here is some source material for the above:

For every 100 women enrolled in US colleges (degree-granting postsecondary institutions) at all levels there are 75 men enrolled. Source: National Center for Education Statistics

For every 100 women enrolled in US graduate schools there are 68 men. Source: Council for Graduate Schools (2020)

For every 100 women who earn bachelor’s degrees from US colleges and universities, there are 73 men. Source: National Center for Education Statistics (2021-2022)

For every 100 females in local jails in the US, there are 614 males. Source: Department of Justice via Wikipedia

For every 100 females in state and federal prisons, there are 1,225 males. Source: Department of Justice

For every 100 females in federal prison, there are 1,331 male prisoners. Source: Federal Bureau of Prisons

For every 100 female military personnel who have been wounded in action during Operation Enduring Freedom, 5,098 men have. Source: Congressional Research Service

For every 100 female military personnel who have been wounded in action during Operation Iraqi Freedom, 4,982 menhave. Source: Congressional Research Service

In July, eitght years ago, Detroit filed for bankruptcy protection. The US was well into an economic expansion, but the expansion had largely bypassed Detroit. The Detroit area unemployment rate was 9.7%, and the Detroit city rate was 17%, among the highest in the nation. Tax income was not sufficient to pay retirement or current employees. The city was riven by corruption and crime, and attendance in school was dismal, less that 25% in some districts, about 55% as an overall average. Kids no longer saw a value in education. After bankruptcy, things started to improve dramatically.

Detroit area unemployment rate, 2005 to 2021.

The largest cause of the problem, and of the solution, in my opinion, was a high Detroit minimum wage that applied before bankruptcy and that was voided by bankruptcy. It was called a “living wage”. In 2013 it was $16/ hour and applied to any business that dealt with the city and did not offer health insurance (see more on the specifics here).The stated purpose was to insure that all workers could support a family of four in some middle-class standard, by one wage-earner working 40 hours per week. It was a view of Detroit family life and economic need that didn’t match Detroit reality. In practice most of Detroit were not 4 person, one wage-earner households. It meant that most Detroiters could not find jobs, since most companies worked in some way with the city. The only workers who could find jobs were those with special skills or political connections. The alternative was criminal business including drug sales, prostitution and burglary. The unemployment rate was 70% among Detroit’s teenagers.

The high minimum wage bought loyalty for Detroit’s political bosses; they gave out jobs for kickbacks, and some went to jail, including the mayor. Most Detroiters could not find jobs, though, and this especially hurt those looking for their first job: the job that would demonstrate that math and spelling were important; that you had to show up on time, dressed clean, and that you were not to insult the customers. High unemployment meant low tax revenue, made worse by high city employment costs for basic services: janitors, secretaries, and mail room personnel. The city was a mess.

When Detroit went bankrupt, among the first changes was to eliminate the $!6/hour living wage for employees and others doing business with the city. This helped bring the city budget into balance, and it brought in residents, businesses, and developers. By January 2020 Detroit’s unemployment rate had fallen to 6%, and Detroit metro unemployment had fallen to 4.2%, the lowest rates on record. Employment gives a motivation to stay in Detroit and to stay in school: there are jobs to be had for those who could add and spell. I covered these improvements here.

Seattle are unemployment rate 2015 to 2021. Seattle’s unemployment rate is now higher than Detroit’s.

Meanwhile, Seattle voted to raise their minimum wage to $15, with the change law taking effect in stages. The law fully came into effect three months ago, in January, 2021. New York voted for similar changes more recently. It is hard to be sure of the effect of the high minimum wage but already it seems to have hit employment. By the latest data, Seattle’s unemployment rate has risen to 6.9%. That’s higher than in Detroit, a real reversal. While unemployment in New York City has yet to rise much, they have seen a drop in rent rates while Detroit has seen a rise. New York’s are also moving to be more out of balance, something that leads to corruption and bankruptcy. We’ll see how this works out.

…And [the leper] shall cover his face to the lip, and call out unclean, unclean… (Lev. 13: 45)

Video and TV-learning has been with us for a long time. It’s called PBS. It’s entertaining, but as education, it sucks. You can see the great courses on DVD too. The great professors teaching great material. It’s entertaining, but as education, they suck.

Consider PBS, the public broadcast system, it was funded 50 years ago and given a portion of the spectrum to be a font for at-distance education. At first they tried showing classroom lectures from the best of professors. Few people watched, and hardly anyone learned. Hardly anyone was willing to do catch every lecture, or do any of the reading or any of the assigned homework. Some did some problems, but only if they already knew the subject, sort of as a refresher . No viewer of record learned enough to perform a trade based on PBS-learnign, nor achieved any academic proficiency that would allow them to publish is a reviewed journal, unless they already had that proficiency. A good question is why, but first lets consider the great DVD lectures in science or engineering . They too have been around for years, but I’ve yet to meet anyone of proficiency who learned that way. Not one doctor, lawyer, or engineer whose technical training came this way. Even Sesame street. My sense is that no one ever learned to read from this, or from the follow-on program reading rainbow, except that they had parental help — the real teachers being the parent. My sense is that all formal education over video is deficient or worthless unless it’s complimented by an in-person, interaction. The cause perhaps we are not evolutionarily developed to connect with a TV image the way we connect with a human.

Education is always hard because you’re trying to remold the mind, and it only works if the student wants his or her mind molded. To get that enthusiasm requires social interaction, peer pressure and the like, and it requires real experience, not phony video. Play is a real experience, and all animals enjoy play. it convinces them they can do things, This stag on a now-empty soccer field is busy developing soccer skills and is rewarded here with a reaching his goal. Without the physical goal there would be no practice, and without the physical practice there would be no learning.

For people, the goals of the goals of the teacher must be made to match those of the student. The teachers goals are that they student should love learning, that he or she should acquire knowledge, and that he or she should be prepared to use that knowledge in a socially acceptable way. For the student, the goals include being praised by peers, and getting girls/ boys, and drinking. Colleges work, to the extent they do, but putting together the two sets of goals. Colleges work best in certain enclaves — places where the student’s statues increases if he or she does well on exams or in class, where he or she can drink and party, but will get thrown out if they do it so much that their grades suffer. Also colleges make sure to have clubs and sports where he or she can develop a socially acceptable way to deal with others. Remove the goals an rewards, and the lessons become pointless, or “academic.”

A cave painting from France. It’s diagrammatic, not artistic. It shows where you stand, how you hold the spear, and where the spear is supposed to go, but the encouragement to do it had to be given in person..

It might be argues that visual media can make up for real experience, and to some extent this is true. Visual media has been used since the beginning, as with this cave painting, but it only helps. You still need personal interaction and real-life experience. An experienced hunter could use the cave picture to show the student where to stand and how to hold the spear. But much of the training had to be social, with friends before the hunt, in the field, watching friends and the teacher as they succeed or fail. And — very important — after the hunt, eating the catch, or sitting hungry rubbing one’s bruises. This is where fine-points are gained, and where the student became infected with the desire to actually do the thing right. Leave this out, and you have the experience of the typical visitor to the museum. “Oh, cool” and then the visitor moves on.

In a world of Zoom learning, there is no feast at the end, no thrill of victory, and no agony of defeat. The students do not generally see each other, or talk to one another. They do not egg each other on, or condemn bad behavior. They do not share stories, and there is no real reward. There is no way to impress your fellow, and no embarrassment if you fail, or fail to work. The lesson does not take hold because we don’t work this way. A result is that US education as we know it is in for a dramatic change, but the details are sill a little fuzzy.

As best I can tell, our universities managers do not realize the failure of this education mode, or the choose to ignore it. If they were to admit defeat, they would lose their job. They can also point to a sort of artificial success, as when an accomplished programmer learns a bit more programming, or when an accomplished writer learns a new trick, but that’s not real education, and it certainly isn’t something most folks would pay $50,000 per year for.

Harvard University claims it will be entirely on-line next year, and that it will charge the same. We will have to see how that works for them. You still get the prestige of Harvard, though you can no longer join the crew team, or piss on the statue of John Harvard. My guess is that some people will put up with it, but not at that price. Why pay $50,000 — the equivalent of over $100/hour when you can get a complete set of DVDs on the material for $100, and a certificate. Without the physical pain or rowing, or the pleasure of pissing, there is no real connection to your fellow student, and a lot of the plus of Harvard is that social connection.

On line education isn’t strange; it just isn’t education.

I expect the big mid tier colleges to suffer even more than the great schools. I don’t expect 50,000 students to pay $40,000 each to go to virtual Indiana State. Why should they? Trade-schools may last, and mini-colleges, those with a few hundred students, that might be able to continue in a version of the old paradigm, and one-on-one or self-learning. This worked for Lincoln, and Washington; for Heraclitus and for Diogenes. Self study and small schools are good for self-reflection and refinement. The format is different from on-line, more question and answer. Some folks will thrive, others will flounder — Not everyone learns the same– but the on-line university will die. $40k of student debt for on-line lectures followed by an on-line, virtual graduation? No, thank you.

The reason that trade schools will work, even in a real of COVID, is they never focussed as much on personal interaction, but more on the interaction between your hands and your work. This provides a sort of reality check that doesn’t exist in typical on-line eduction. If your weld breaks, or your pipe leaks, you see it. Non-trade school, on-line eduction suffers by comparison, since there is no reality in the material. Anything can be shown on screen. My undergrad college, a small one, Cooper Union, used something of a trade school approach. For example, you learned control theory while sitting underneath a tank of water. You were expected to control the water height with a flow controller. When you got the program wrong, the tank ran dry, or overflowed, or did both in an oscillatory way. I can imagine that sort of stuff continuing during COVID lockdowns, but not as an on-line experience.

It seems to me that the protest and riots for Black Lives serve as a sort of alternative college, for the same type of person. It relieves the isolation, and provides a goal. My mother-in-law spent her teenage years in Ravensbruk concentration camp, during the holocaust, and my father-in-law survived Auschwitz. They came out scarred, but functional. They survived, I think, because of a goal. A recognition that the they were alive for a reason. My mother-in-law helped her sister survive. For many these days, ending racism by, tearing down statues is the goal. The speeches are better than in on-line colleges., you get the needed physical and social interaction, and you don’t spend $50,00 per year for it.

Robert Buxbaum July 24, 2020. These are my ramblings based in part on my daughter’s experience finishing college with 4 months of on-line eduction. The next year should see a shake-out of colleges that are not financially sound, I expect.

The following is an oldish logic joke. I used it to explain a conclusion I’d come to, and I got just a blank stare and a confused giggle, so here goes:

Three logicians walk into a bar. The barman asks: “Do all of you want the daily special?” The first logician says, “I don’t know.” The second says, “I don’t know.” The third says, “yes.”

The point of the joke was that, in several situations, depending on who you ask, “I don’t know” can be a very meaningful answer. Similarly, “I’m not sure.” While I’m at it, here’s an engineering education joke, it’s based on the same logic, here applied:

A team of student engineers builds an airplane and wheel it out before the faculty. “We’ve designed this plane”, they explain, “based on the principles and methods you taught us. “We’ve checked our calculations rigorously, and we’re sure we’ve missed nothing. “Now. it would be a great honor to us if you would join us on its maiden flight.”

At this point, some of the professors turn white, and all of them provide various excuses for why they can’t go just now. But there is one exception, the dean of engineering smiles broadly, compliments the students, and says he’ll be happy to fly. He gets onboard the plane seating himself in the front of the plane, right behind the pilot. After strapping himself in, a reporter from the student paper comes along and asks why he alone is willing to take this ride; “Why you and no one else?” The engineering dean explains, “You see, son, I have an advantage over the other professors: Not only did I teach many of you, fine students, but I taught many of them as well.” “I know this plane is safe: There is no way it will leave the ground.”

Robert Buxbaum, November 2i, 2018. And one last. I used to teach at Michigan State University. They are fine students.

In my time in college, as a student, grad student, and professor, I ran into quite a few geniuses and quite a few weirdos. Most of the geniuses were weird, but most of the weirdos were not geniuses. Many geniuses drank or smoked pot, most drunks and stoners were stupid, paranoids. My problem was finding a reasonably quick way to tell the geniuses from the nuts; tell Einsteins from I’m-stoned.

Only quick way I found is by their friends. If someone’s friends are dullards, chances are they are too. Related to this is humility. Most real geniuses have a body of humility that can extent to extreme self-doubt. They are aware of what they don’t know, and are generally used to skepticism and having to defend their ideas. A genius will do so enthusiastically, happy to have someone listen; a non genius will bristle at tough questions, responding by bluster, bragging, name dropping, and insult. A science genius will do math, and will show you interesting math stuff just for fun, a nut will not. Nuts will use big words will have few friends you’d want to hang with. A real genius uses simple words.

Another tell, those with real knowledge are knowledgeable on what others think (there’s actually a study on this). That is, they are able to speak in the mind-set of others, pointing out the logic of the other side, and practical differences where the other side would be right. There should be a clear reason to come on one side or the other, and not just a scream of frustration that you don’t agree. The ability to see the world through others’ eyes is not a proof they are right — some visionary geniuses have been boors, but it is a tell. Besides boors are no fun to be with; they are worth avoiding if possible.

And what of folks who are good to talk to; decent, loyal, humble, and fun, but turn out to be not-geniuses. I’d suggest looking a little closer. At the worst, these are good friends, boon companions, and decent citizens — far more enjoyable to deal with than the boors. But if you look closer, you may find a genius in a different area — a plumbing genius, or a police genius, or a short-order cook genius. One of my some-time employees is a bouncer-genius. He works as a bouncer and has the remarkable ability to quite people down, or throw them out, without causing a fight — it’s not an easy skill. In my political work trying to become drain commissioner, I ran into a sewage genius, perhaps two. These are hard-working people that I learn from.

People make the mistake of equating genius with academia, but that’s just a very narrow slice of genius. They then compound the mistake by looking at grades. It pays to look at results and to pay respects accordingly. To quote an old joke/ story: what do you call the fellow who graduated at the bottom of his medical school class? “Doctor” He or she is a doctor. And what do you call the fellow who graduated at the bottom of his law school class? “your honor.”

{kind=link}